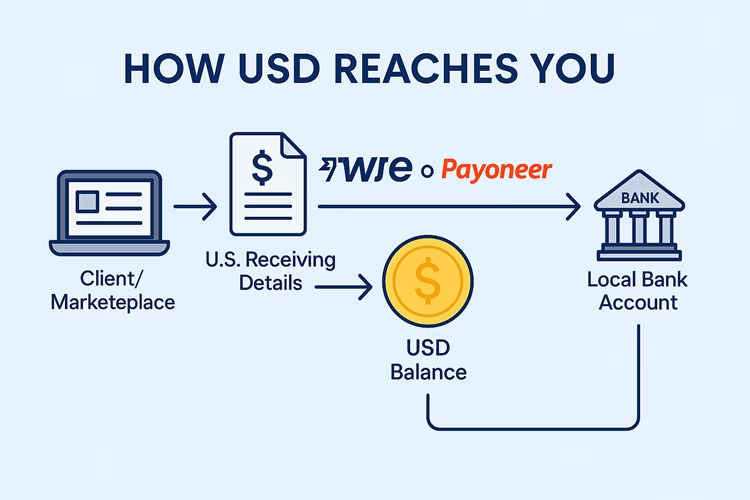

How does receiving USD via a U.S. bank account work?

If you live outside the U.S. but earn in USD, many payment platforms need a U.S. bank account — without actually opening a physical U.S. bank account. Here’s the simple flow:

Open a U.S. receiving account. Services like Wise and Payoneer provide local-looking U.S. bank details (routing + account numbers). You can open a bank account with them for free. Payers (clients, marketplaces) send USD to the account via ACH or a domestic U.S. transfer.

Funds land in your multi-currency balance. The platform receives the USD on your behalf and credits it to your account balance. This keeps the money in USD until you withdraw it (via Wise) or it is withdrawn automatically for you (via Payoneer).

Convert or hold. You can either keep USD in the multi-currency wallet or convert it to your local currency using the platform’s exchange rate. Conversion may include a small margin above the mid-market FX rate.

Withdraw to your local bank. When you request a withdrawal, the provider sends the funds to your local bank using local rails (e.g., local ACH, Faster Payments) or international rails (SWIFT). Withdrawal times and fees vary depending on the provider and your country of residence.

Key things to check: When considering payment options, it is important to verify if the receiving details are valid U.S. routing and account numbers. You should also confirm which types of incoming payments are accepted, such as ACH or wire transfers. Be aware of any Know Your Customer (KYC) or verification requirements, as well as the limits on transfers per transaction and monthly. Additionally, take note of the provider’s conversion fees and transfer times. These technical differences can significantly impact costs, speed, and the marketplaces that will accept your receiving information.

Pros and Cons

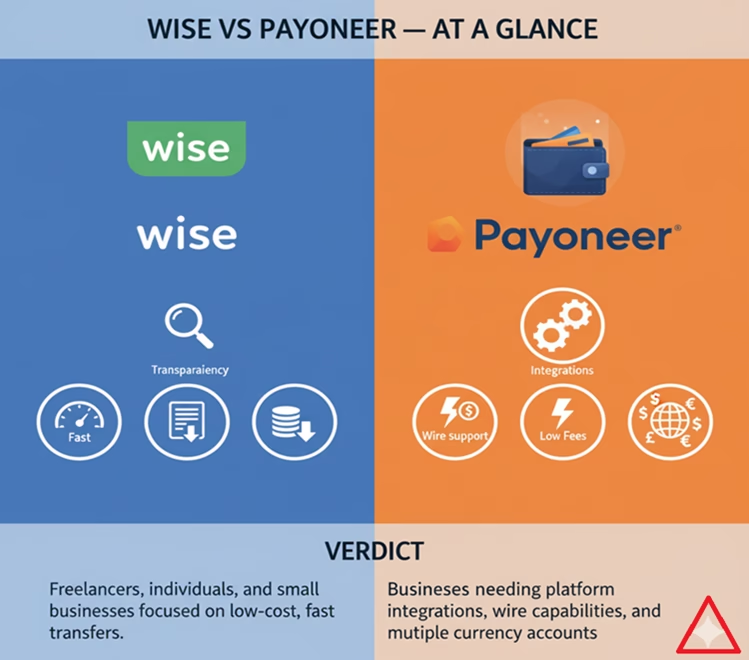

After comparing Wise and Payoneer across features like fees, speed, and integrations, here’s a clear breakdown of each platform’s key advantages and disadvantages to help you decide which one fits your online earning needs best.

Wise (formerly TransferWise)

Pros

- Transparent Fees: Uses the real mid-market exchange rate with a small, clearly shown fee — no hidden markups.

- Fast Transfers: Local withdrawals are often completed within hours or the same day.

- Low Conversion Costs: Ideal for freelancers, affiliate marketers, and remote workers.

- Simple User Experience: Clean dashboard, real-time tracking, and easy-to-understand pricing.

- Multi-Currency Support: Hold and convert between 40+ currencies effortlessly.

- Local Bank Withdrawals: Offers direct transfers to many countries’ local banking networks, reducing SWIFT charges.

Cons

- No USD Wire Transfer Support: Only supports ACH transfers for USD — not ideal for clients using wire payments.

- Limited Marketplace Integrations: Some marketplaces may not support Wise.

- No Mass Payout Feature: Lacks tools for managing large-scale or recurring business payments.

✅ Best For: Freelancers, consultants, and remote workers who want low-cost USD-to-local transfers with full fee transparency.

Payoneer

Pros

- Supports ACH and Wire Transfers: Allows you to receive USD payments from almost any U.S. client or company.

- Marketplace Integrations: Seamlessly connects with Upwork, Fiverr, Amazon, Airbnb, and many others, enabling automatic payouts.

- Global Payment Service: Lets you receive payments in multiple currencies (USD, EUR, GBP, etc.) using local bank details.

- Prepaid MasterCard Option: Spend funds directly online or withdraw from ATMs worldwide.

Cons

- Higher Conversion Fees: Currency conversions typically include a 2–3% margin above the mid-market rate.

- Longer Transfer Times: 1–3 business days.

- Complex Fee Structure: Some incoming payments, card transactions, or withdrawals may incur hidden or variable fees.

✅ Best For: Freelancers and businesses receiving payments from marketplaces, U.S. companies, or multiple currencies who need wide payout compatibility.

At a Glance: Which One Should You Choose?

| Category | Best Choice |

|---|---|

| Lowest Fees | Wise |

| Marketplace Compatibility | Payoneer |

| Fast Withdrawals | Wise |

| Receiving USD via Wire | Payoneer |

| Transparency & Ease of Use | Wise |

| Business & Bulk Payments | Payoneer |

Disclosure: We are partners or associates of Amazon and other top brands. We may earn a small amount from qualifying purchases without increasing the price. Please read our full affiliate disclosure here.